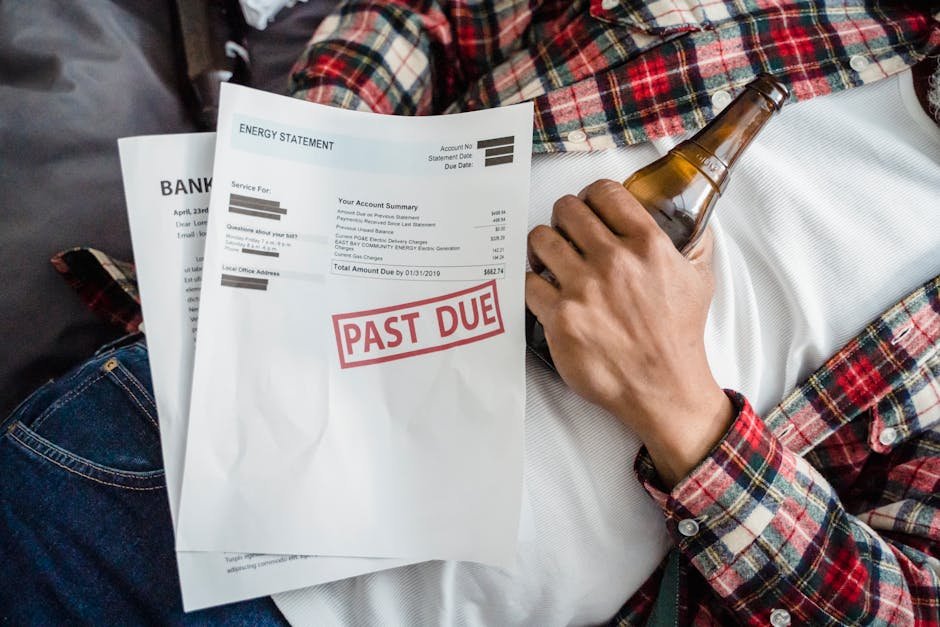

Renee from Cleveland was three weeks into her psychiatric inpatient stay when she got the first bill in the mail: $87,400 from the hospital, $12,200 from the attending psychiatrist, and another $4,800 from the lab. Her insurance had paid most of it, but her share alone was $14,600 after the out-of-pocket maximum, and she’d already drained her emergency fund covering rent during her medical leave. By the time her partner suggested talking to a bankruptcy attorney, the collections calls had started, two of her credit cards had been closed by the issuers, and she was skipping psychiatric follow-up appointments because she was terrified of adding to the debt. The attorney she eventually met with explained something nobody had told her: medical debt is the leading cause of bankruptcy in the United States, the automatic stay would stop the calls instantly, and Chapter 7 would discharge most of the bills without affecting her ongoing treatment. Renee filed two months later and was back in therapy within weeks. Understanding bankruptcy mental health insurance protections changed her life because she finally stopped choosing between treatment and solvency.

Medical Debt Is the Number One Cause of Bankruptcy

Multiple studies, including analyses by the American Journal of Public Health and data compiled by the Census Bureau and the Agency for Healthcare Research and Quality (AHRQ), have consistently identified medical bills as the leading or near-leading cause of personal bankruptcy filings in the United States. Estimates range from 60% to 67% of bankruptcies involving significant medical debt as a contributing factor. Mental health and substance use treatment are particularly devastating because residential and inpatient stays can run $30,000 to $100,000 or more for a single episode, and many patients face multiple episodes over a lifetime. Even with insurance, the cost-sharing math (deductibles, coinsurance, out-of-pocket maximums) can wipe out savings and push families into debt that takes years to recover from.

The bankruptcy mental health insurance intersection is uniquely complex because mental illness often comes with employment disruption, which means coverage gets lost at the same time bills are piling up. The good news is that bankruptcy law was designed to give honest debtors a fresh start, and the protections available to people overwhelmed by mental health debt are stronger than most realize.

Chapter 7 vs Chapter 13: Two Different Tools

The two consumer bankruptcy chapters serve different needs. Chapter 7 is a liquidation bankruptcy that discharges most unsecured debts (including medical bills, credit cards, and personal loans) in roughly four to six months. To qualify, you must pass a means test that compares your income to the median for your state. Chapter 7 doesn’t restructure your debts; it eliminates them, with the trade-off that non-exempt assets can be sold to pay creditors. For most filers with mental health debt, exemptions cover all their assets and the trustee finds nothing to liquidate.

Chapter 13 is a reorganization that puts you on a 3-to-5-year repayment plan based on disposable income. It’s used by debtors who don’t qualify for Chapter 7 (income above the median), who want to save a home from foreclosure, or who have non-exempt assets they’d lose in a Chapter 7. Mental health debt is treated as general unsecured debt in both chapters, but Chapter 13 plans typically pay only a fraction of unsecured debt before discharging the rest at the end of the plan. The uscourts.gov bankruptcy basics page explains the procedural differences in detail.

The Automatic Stay Stops Collections Instantly

The moment you file a bankruptcy petition, an automatic stay goes into effect under 11 U.S.C. Section 362. The stay legally prohibits creditors from continuing collection actions, including phone calls, letters, lawsuits, wage garnishments, bank levies, and credit reporting changes. For someone in mental health crisis, this protection is enormous. Collections harassment is a known trigger for anxiety, depression, and self-harm ideation, and the stay creates a legal shield that gives debtors space to stabilize. Hospitals and medical providers must stop billing activity immediately upon receiving notice of the filing, even if their internal collections department hasn’t been formally notified yet.

Violations of the automatic stay carry penalties, including damages and attorney fees. If a creditor calls or sends a bill after being notified of the filing, your bankruptcy attorney can file a motion for sanctions. Stopping medical debt collection harassment is one of the most immediate benefits of filing, and many clients describe the silence after the stay takes effect as the first peaceful moment they’ve had in months.

Exempting Future Treatment From the Bankruptcy Estate

When you file bankruptcy, all your assets become part of the bankruptcy estate, but exemptions allow you to protect specific categories from liquidation. Federal exemptions and state exemptions vary, but most jurisdictions protect tools of the trade, retirement accounts, vehicles up to a certain value, household goods, and a wildcard exemption that can be applied to anything. The question for mental health debtors is how to protect ongoing treatment costs and the financial resources needed to access care.

- Health Savings Account (HSA) balances are protected in many states (varies by state law, with some treating HSAs as exempt retirement-style accounts)

- Future earnings after the filing date are not part of the estate in Chapter 7

- Disability benefits (SSDI, SSI, private disability insurance) are typically exempt

- Pre-paid medical retainers or therapist deposits may be exempt under wildcard exemptions

- Health insurance premium payments after filing are not subject to estate claims

COBRA Continuation During Bankruptcy

If you’ve lost a job and are continuing health coverage through COBRA, the premiums you pay are treated as ongoing expenses, not pre-petition debts. You can continue COBRA coverage while in bankruptcy, and the premiums are typically considered necessary medical expenses in Chapter 13 budget calculations. The catch is that COBRA premiums are expensive (often $700-1,500 per month for individual coverage) because they include the employer’s portion plus a 2% administrative fee. For a debtor on the edge financially, COBRA can be unsustainable, and switching to a marketplace plan with subsidies through a Special Enrollment Period (loss of coverage) is often a better strategy.

Bankruptcy filing itself does not trigger a Special Enrollment Period for marketplace coverage, but loss of employer coverage (often the precipitating cause of bankruptcy) does. Coordinating the timing of COBRA election, marketplace enrollment, and bankruptcy filing requires planning, and a bankruptcy attorney experienced with healthcare can be invaluable here.

Dischargeable Debt vs Ongoing Treatment Costs

Bankruptcy discharges debts incurred before the filing date. Treatment received after filing is your responsibility going forward. This means that if you’re still in residential treatment when you file, the bills accruing post-petition are not part of the bankruptcy estate. Practically speaking, most patients wait until after discharge from inpatient or residential care before filing, which lets them include the entire episode of care in the bankruptcy. Long-term outpatient psychiatry, ongoing therapy, and medication costs are not affected by the filing because they’re future expenses, paid as you go.

Some debts are not dischargeable in bankruptcy: federal student loans (with rare exceptions), recent income taxes, child support, and debts arising from fraud or willful injury. Medical debt does not fall into any of these non-dischargeable categories. Even disputed medical bills, denied insurance claims, and bills from out-of-network providers are dischargeable. Disputing surprise medical billing is a separate process that may resolve some bills entirely without bankruptcy, and savvy attorneys explore those options before filing if time allows.

Hospital Charity Care and Bill Reduction Before Filing

Before filing bankruptcy, attorneys often recommend exhausting charity care and bill reduction options because they preserve more of your resources and avoid the long-term credit consequences of filing. Nonprofit hospitals are required by IRS Section 501(r) regulations to maintain financial assistance policies, and most for-profit hospitals offer similar programs because uncompensated care is often written off anyway. Income at or below 200% of the Federal Poverty Level usually qualifies for full or near-full forgiveness, with sliding-scale reductions extending to 400% FPL at many institutions.

The application process varies by hospital but typically requires income documentation, asset disclosure, and a written request. Mental health units within general hospitals are usually covered by the hospital-wide charity care policy, but freestanding psychiatric and addiction treatment facilities may have separate (or no) charity programs. Always ask. The financial counselor’s job is to find a way for you to pay something rather than nothing, and they often have authority to discount bills 50-80% before any application is even processed.

Finding a Bankruptcy Attorney Who Understands Mental Health

Most consumer bankruptcy attorneys handle medical debt cases routinely, but few specialize in the mental health intersection. Look for attorneys who advertise medical bankruptcy specifically, who have experience with disability claims (many mental health bankruptcies involve simultaneous SSDI applications), and who understand the timing of treatment relative to filing. Initial consultations are usually free, and a good attorney will ask about your treatment history, income, employment status, and goals before recommending a chapter. Cost varies, but Chapter 7 typically runs $1,000-2,500 in attorney fees plus the $338 court filing fee, while Chapter 13 fees are paid through the plan and run $3,000-5,000 in most jurisdictions.

The National Association of Consumer Bankruptcy Attorneys (NACBA) maintains a directory, and legal aid organizations in most states offer free or low-cost bankruptcy representation for qualifying low-income debtors. Coordinating bankruptcy with disability and benefits planning is something specialists handle daily, and the right attorney can save you years of stress.

The CFPB Medical Debt Credit Reporting Changes

The Consumer Financial Protection Bureau finalized a rule in early 2025 that removed medical debt from consumer credit reports for most purposes, with the major credit bureaus (Equifax, Experian, TransUnion) implementing changes through 2025 and 2026. The rule prohibits lenders from considering medical debt in underwriting decisions for mortgages, auto loans, and credit cards. Implementation has been phased and litigation has affected timelines, so check the consumerfinance.gov page for the current status. Even with the changes, hospital collections agencies can still pursue debts through legal channels, file lawsuits, and obtain judgments. The CFPB rule limits credit reporting impact, not collections activity itself.

For people who would have considered bankruptcy primarily to clean up their credit reports, the CFPB rule may make filing less necessary. However, for people facing active lawsuits, wage garnishments, or overwhelming debt loads, the automatic stay and discharge of bankruptcy still offer protections that the credit reporting rule alone cannot.

Frequently Asked Questions

Will bankruptcy affect my ability to keep seeing my therapist or psychiatrist?

No. Ongoing treatment after the filing date is your responsibility and continues as normal. Pre-petition debts are discharged, but your existing therapeutic relationships and prescription continuity are not interrupted by the legal filing.

Can I keep my health insurance during bankruptcy?

Yes. Health insurance premiums are considered necessary expenses in both Chapter 7 and Chapter 13. You can continue marketplace coverage, COBRA, or employer-sponsored coverage throughout the bankruptcy process.

Does bankruptcy discharge unpaid insurance copays and deductibles?

Yes. Patient responsibility amounts owed to providers are general unsecured debts and are discharged like any other medical bill. The only exception is debts incurred through fraud, which doesn’t apply to legitimate cost-sharing.

How long does bankruptcy stay on my credit report?

Chapter 7 remains on your credit report for 10 years from the filing date. Chapter 13 remains for 7 years. The impact on credit scores diminishes over time, and many filers see scores recover meaningfully within 18-24 months by establishing new positive credit.

Should I file bankruptcy or negotiate with the hospital first?

Negotiation first, almost always. Charity care, prompt-pay discounts, and payment plans can resolve significant portions of debt without filing. Bankruptcy makes sense when total debt across all sources exceeds your ability to negotiate or pay over a reasonable timeframe.

The Bottom Line

Bankruptcy is not a moral failing. It’s a legal tool created specifically to help honest debtors recover from financial catastrophes that aren’t entirely their fault, and mental health crises are among the clearest examples. The automatic stay stops collections immediately, Chapter 7 discharges most medical debt within months, exemptions protect ongoing treatment resources, and health insurance continues uninterrupted. Combined with hospital charity care, the No Surprises Act, and the CFPB credit reporting changes, the legal landscape for mental health debt has shifted significantly in patients’ favor over the past few years. If medical bills are forcing you to skip treatment, the cost is too high. Talk to a bankruptcy attorney before the situation gets worse.

Crisis Resources

If you or someone you know is in mental health crisis, call or text 988 for the Suicide and Crisis Lifeline, available 24/7 in the United States. Financial stress can intensify suicidal ideation, and help is available immediately.

This article is for informational purposes only and does not constitute legal, financial, or medical advice. Bankruptcy law and credit reporting rules vary by jurisdiction and change frequently. Consult a licensed bankruptcy attorney in your state before making decisions about filing or debt management.